Mandatory Flood Insurance

One of the things that’s confusing for homeowners is the question of mandatory flood insurance. As a homeowner, do I need flood insurance? The question really lies in where your home sits in relation to FEMA’s flood zone maps. That is the key difference between mandatory flood insurance, or not needing to carry it at all. Having said that, keep in mind that almost a third of all flood insurance claims happen in low to moderate risk zones, and normal homeowner’s insurance doesn’t cover flooding events in their list of covered perils.

Mandatory Flood Insurance basic concepts:

Where is my house located?

Luckily, the public has access to FEMA’s flood risk maps, which can be accessed here.

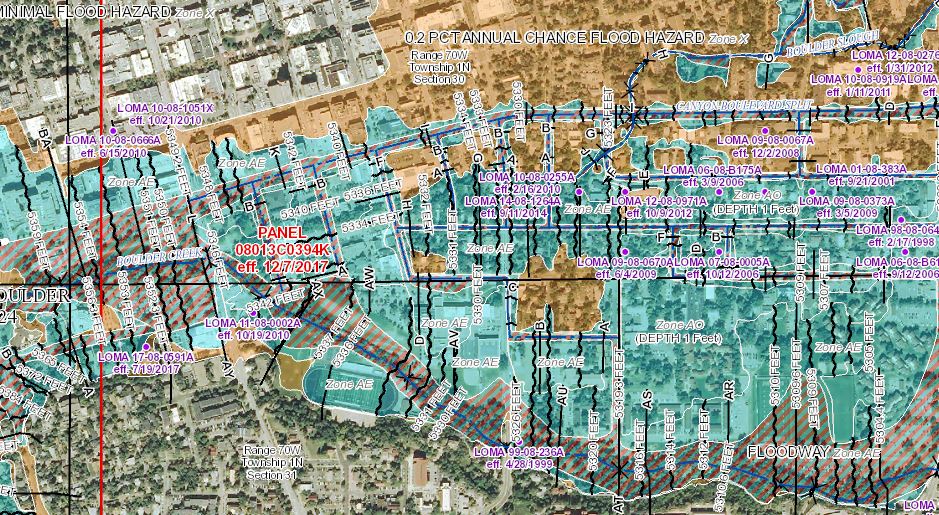

You will want to pull up the location of your home and see if it resides in a Special Flood Hazard Area (SFHA) – these are commonly marked on the map by “A” zones. “X” zones are a lower (.02%) annual risk of flooding, verses the A risk (traditionally called a 100 year flood plain, which represents of a 1% chance of a flood every year)

Take for example the picture below. Now, this flood zone hazard map can be a little daunting and difficult to read to the untrained eye, but as a basic concept – if your home were covered even partially by the blue shading, that would mean you’re in an AE zone or special flood hazard area, and mandatory flood insurance would be the result. Now, remember it’s not the government mandating you have the insurance, but your mortgage company. Because they have a financial stake in your property until the loan is fully paid off, they will be the ones requiring that you as the owner carry this mandatory flood insurance.

Having noted this, once your mortgage is paid off, you won’t have mandatory flood insurance, but it’s still probably a good idea to carry it. If you reside in a home that is in the orange shaded area, this would be an X zone representing the lower flood risk – but there’s still a flood risk. Take for example the events of Hurricanes Irma and Harvey – Harvey in particular, 80% of the victims of the event didn’t carry flood insurance. Want to read more on that? Check out this article from USA Today.

So, yes – mandatory flood insurance is a thing that can be imposed on you by your lender. But even if flood insurance isn’t mandated, it’s a pretty darn good idea to carry it even if you think your home will “never flood”.

Non Mandatory Flood Insurance

I personally live in a very dry state, Colorado. There’s no active streams or rivers anywhere near my home, only an old dry gulch. Below are some images from a video I shot in the spring of 2016 outside our home. A normally dry area was inundated with water just from one day of heavy rain. It can happen anywhere! So, if you are looking to get flood insurance at an affordable rate, you can get a quote with Save Flood Insurance Agency Inc today.